The tax framework in Uruguay is structured around both direct and indirect taxes, operating mostly under the principle of territoriality.

Main taxes in Uruguay related to business activity

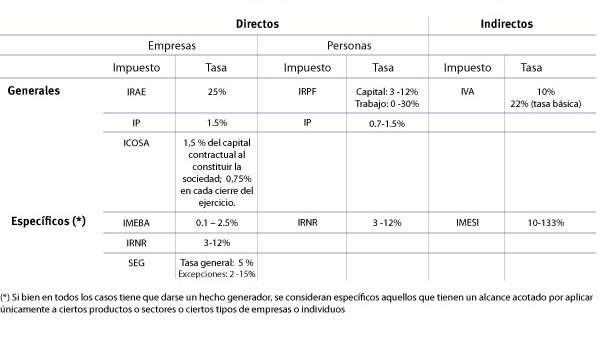

In the business area, the most relevant direct taxes are the Tax on Income from Economic Activities (IRAE), with a rate of 25%, and the Wealth Tax (IP), with a rate of 1.5%. Taxation is applied exclusively on income of Uruguayan origin, without recognition of credit for taxes paid abroad, unless there are double taxation agreements.

For individuals, Personal Income Tax (IRPF) is the main direct tax. This tax, of a personal and direct nature, is levied on the income of residents in Uruguay, and a progressive rate is applied according to income.

Contáctanos para más información

Income obtained in Uruguay by non-resident individuals or entities without permanent presence in the country is subject to Non-Resident Income Tax (IRNR), with rates varying between 7% and 12% depending on the nature of the income.

Indirect taxes include VAT and IMESI. The general VAT rate is 22%, with a reduced rate of 10% for certain goods and services. Exports and most agricultural products benefit from a zero rate, allowing the tax credit to be refunded.

The Internal Specific Tax (IMESI) affects the first sale of certain products by producers or importers, excluding exports. The main products subject to this tax include fuels, tobacco, beverages, cosmetics and vehicles, with variable rates.

When considering investments in Uruguay, it is important to take into account the country’s incentive system, which offers, among other benefits, the possibility of deducting the investment made from IRAE taxable income.

Uruguayan tax regime

General characteristics

- The tax framework in Uruguay is composed of both indirect and direct taxes, with the source criterion predominating as the general guiding rule. Indirect taxes are the largest contributors to tax revenues.

- The most significant taxes affecting the business sector include the Value Added Tax (VAT), the Wealth Tax (IP) and the Tax on Income from Economic Activities (IRAE).

- Income is subject to taxation either through IRAE, Personal Income Tax (IRPF) or Non-Resident Income Tax (IRNR), depending on the ownership of the income.

- Free zone operators are tax exempt in most cases, enjoying considerable tax exemption, with some specific exceptions.

Main taxes in Uruguay

Tax on Income from Economic Activities

The Tax on Income from Economic Activities (IRAE) is an annual tax liability that applies 25% on net income of Uruguayan origin, derived from any type of economic activity. Uruguayan source income is considered to be income derived from activities carried out, assets located or economic rights used within Uruguayan territory. Profits from agriculture and livestock are also subject to IRAE. However, under certain circumstances, taxpayers may elect to be taxed under the IRAE or the Tax on the Disposal of Agricultural Goods (IMEBA), which applies to the sale of certain agricultural products.

It should be noted that there are exemptions available under Law No. 16,906 on Investment Promotion, as well as various incentive regimes for investment in Uruguay, which are explained in more detail in the chapter on Investment Promotion Regimes.

Personal Income Taxes

The Personal Income Tax (IRPF) is a direct and personal tax levied on income obtained by individuals resident in Uruguay. Residents are considered to be those individuals who spend more than 183 days in the country during the calendar year, who have in Uruguay the main core of their activities or the center of their vital or economic interests. This tax operates under a dual system that differentiates between income generated by capital, with rates varying between 7% and 12%, and income generated by labor, subject to progressive rates of up to 36%.

The tax is determined annually as of December 31, although there are advance and withholding mechanisms applicable to different types of income.

Non-Resident Income Taxes

The Non-Resident Income Tax (IRNR) is an annual tax levied on Uruguayan source income obtained by non-resident individuals or entities that do not have a permanent establishment in the country. The applicable rates vary between 7% and 12% depending on the income class. If the beneficiary is an entity from a country with low or no taxation, or benefits from a favorable tax regime, the rate is increased to 25% (except in the case of dividends, which have a rate of 7%). Generally, this tax is withheld by local companies that pay or credit subject income to the nonresident. In the absence of a withholding agent, the taxpayer must designate a representative in Uruguay and pay the tax directly.

Contáctanos para más información

Wealth Tax

The Property Tax (IP) is an annual levy on the net assets in the country, after deducting certain liabilities, at the close of the fiscal year. The rate is 2.8% for banks and financial institutions and 1.5% for other legal entities. Entities resident in low or no-tax jurisdictions are subject to a 3% tax rate. Individuals pay IP at progressive rates ranging from 0.2% or 0.7% to 0.5% or 1.5%, depending on whether they are residents or non-residents. There is a gradual reduction of these rates with a view to unifying them at 0.10%. The minimum exemption for individuals is set by the government and is approximately USD 115,000.

Value Added Tax

Value Added Tax (VAT) is levied on the internal transfer of goods and the rendering of services in Uruguay, as well as on the importation of goods and the value added in real estate constructions. Exports are subject to a 0% tax rate, which means that they are not effectively required to pay this tax. The standard VAT rate is 22%, with a reduced rate of 10% applied mainly to essential goods and medicines, along with a variety of goods and services that are exempt from the tax.

Since August 2015, following the policy of financial inclusion and the use of electronic means of payment, the VAT rate for transactions of goods and services to final consumers was decreased to 20%, provided that the payment is made through debit cards or electronic money methods.

Internal Specific Tax

The Internal Specific Tax (IMESI) applies to the first sale of certain products by producers and importers in the local market, such as cigarettes, alcoholic beverages, soft drinks and cosmetics, among others. Exports of these products are exempt from this tax. The IMESI rate is variable and is established by the Executive Branch within the limits determined by law.

Taxation of companies (direct taxes)

- The taxable income corresponds to the effective net income adjusted to local currency, with specific corrections to reflect the inflationary impact.

- Dividends obtained from entities resident in the country are not subject to taxation.

- Capital gains arising from investments within Uruguay are subject to taxation.

- Interest paid to non-resident entities on loans is deductible within certain parameters and is generally subject to withholding tax.

- The Wealth Tax (IP) and the Tax on Income from Economic Activities (IRAE) are not deductible as expenses.

Dividends sent abroad are subject to IRNR withholding tax, particularly when they derive from income that has been subject to IRAE taxation in the hands of the originating entity. - The accumulated taxable income subject to IRAE (which is not reinvested in fixed assets, intangible assets or in participations in resident entities, or which is not destined to increase gross operating capital) and which are at least four fiscal years old, are treated as deemed dividends. These are subject to IRNR or IRPF, receiving the same tax treatment as dividends effectively distributed.

- Debit balances related to imports, loans and foreign currency deposits held with foreign counterparties are exempt from IP.

Taxation of individuals (direct taxes)

Residents in Uruguay are subject to Personal Income Tax (IRPF). In addition, they must contribute to the Wealth Tax if their wealth within the country exceeds the exempt threshold, which is established annually by the Executive Branch. For individuals, this exemption limit is approximately US$115,000, and this amount is doubled for families.

Individual Income Tax (IRPF)

Personal Income Tax is levied on the income of natural persons residing in Uruguay. A tax resident is considered to be a person who spends more than 183 days a year in the country, whose main core of activities or vital or economic interests are located in Uruguay. In the absence of proof of tax residence in another country, tax residence is attributed by center of economic interest when the individual: (i) owns real estate investments in the country valued at more than 15 million Indexed Units (UI), which is equivalent to about 1,670.000 U.S. dollars, (ii) has a direct or indirect participation in a company valued at more than 45 million UIU (approximately 5,015,000 U.S. dollars) and such company carries out activities or projects considered of national interest according to Law No. 16,906 on Investment Promotion, (iii) invests in real estate valued at more than 3.500,000 UIU (approximately US$390,000), provided that the investment is made after July 1, 2020 and resides in Uruguay for at least 60 days per year, or (iv) participates directly or indirectly in an enterprise with an investment exceeding 15 million UIU (approximately US$1,670,000), provided that such investment is made after July 1, 2020 and results in the creation of at least 15 full-time jobs throughout the year, without implying a reduction of employees in associated enterprises.

This tax is calculated annually and, as a general rule, is settled as of December 31 of each year. This does not exclude the possibility of making payments on account and withholdings on different types of income.

Contáctanos para más información

Taxation of individuals’ assets

The wealth tax applies to the assets of individuals, families and undivided inheritances, calculated on the value of assets located in Uruguay, after deduction of certain liabilities. Only those goods that are located, invested or economically used within the country are considered for this tax.

Individual estate tax rates are progressive and range from 0.2% or 0.7% to 0.5% or 1.5%, depending on whether the owner is a resident or non-resident of the country. There is an exemption threshold for single individuals of around US$115,000, and this amount is doubled for families.

Individuals with tax residence outside Uruguay, as well as foreign legal entities, are not required to pay this tax in relation to export balances, loans and deposits made to residents in Uruguay.

The assets of individuals, families and undivided estates are valued at market price, with certain exceptions, especially in the case of real estate, whose values are periodically fixed by the State.

The following assets are exempt from tax:

- Holdings, such as shares, in entities that already pay this tax and in financial entities engaged exclusively in securities brokerage operations located outside Uruguay.

- Public debt securities.

- Deposits in bank accounts of individuals (although these are considered in the valuation of household goods and furniture).

- The liabilities that can be deducted are mainly the annual average of debts contracted with local banks and only the amount that exceeds the total of the exempt assets plus the assets located outside Uruguay can be deducted.

Taxation of Non-Resident Income

Income generated in Uruguay by non-resident individuals or entities that do not have a permanent establishment in the country are subject to Non-Resident Income Tax (IRNR).

The IRNR is applied at rates ranging from 7% to 12%, varying according to the nature of the income, or 25% in cases where the entity is from a country with a low or zero taxation regime, except for dividends, whose rate is 7%.

IRNR is a tax levied on Uruguayan source income received by non-resident individuals and entities without a permanent establishment in the country.

This tax applies to all types of income acquired by taxpayers, including business income, capital gains, labor income and capital gains. Uruguayan source income is considered to be income derived from activities carried out in Uruguay, assets located in Uruguayan territory and rights economically used within the country. Also included in this category is income from technical and advertising services rendered from abroad to entities obliged to pay IRAE (under certain conditions), as well as income from rental, assignment of sports, image and similar rights of athletes registered in Uruguayan sports clubs, and those derived from intermediation activities related to these.

Value Added Tax

The value added tax has a standard rate of 22%, with a reduced rate of 10% that applies exclusively to certain goods and services.

Export operations and most agricultural product transactions benefit from a 0% rate, in which case the tax credit related to such activities is refunded.

In addition to being the largest contribution to state revenues, the main purpose of the value added tax is to impose a tax on the internal consumption of goods and services, thus avoiding the generation of imbalances in the commercial sphere. It is intended that this tax does not discriminate against imports as compared to domestic production, nor with respect to the number of entities participating in the economic process or their level of vertical or horizontal integration.

Contáctanos para más información

Taxpayers required to pay VAT

All entities that are liable for IRAE are also liable for VAT. This tax also extends to individuals and independent personal service providers.

Links of interest: